Budgeting for People Who Hate Budgeting

Tracking one’s spending sucks. I don’t believe someone living above their means is a failure in any way. That’s because humans have no reason to have that as an innate skill. That being said, I’ve spent many years helping friends with money matters because I’m one of those oddballs who do.

From those experiences, I know without a doubt that someone who struggles with living within their means should NOT be creating a typical budget (like you’d find on Mint.com or similar sites). I’m talking about the kind where you have some set amount you’re allowed to spend each month for each category of spending (e.g. Food, Clothing, etc). Even the apps/websites who try to automatically categorize your transactions aren’t perfect and what you end up with will feel like an accounting job. I’ve yet to meet someone who struggles with their finances and then succeeds at sticking to that type of budget for any meaningful amount of time. But I have seen methods which almost always work to keep someone aware of their spending without the burnout.

Here are 3 ways real humans can excel at budgeting.

1. Define Your Reason

Often, people struggle to budget because they prefer to live in the now. They aren’t natural marshmallow savers and nothing in the world is going to change that. That’s why having a concrete use for the money you’re saving is so important. Saying that you want to stop living paycheck to paycheck isn’t enough. Saving techniques are a whole other article, but a good start is that your reason should have the following characteristics:

Measurable

Rather than “I want an emergency buffer”, come up with something like “I want to save $1,000 for emergency car maintenance”

Attainable

“I need $50,000 for the downpayment on my first house” isn’t realistic if you’re struggling to make ends meet. Try something closer to earth such as “I want to save $1,000 or one month’s rent” so I can focus on bigger housing goals in the future.

Time-Based

If you don’t have a deadline, it might never happen. Instead of “I’d like to replace my car someday”, try “I want to save $3,000 down for a car by January 1st of next year”.

Having a clearly defined reason to live within your means helps you when you’re struggling to keep your spending in check. Whatever your reason is, make sure it’s in writing where you can see it often.

2. “Need” Isn’t Relative and You “Deserve” What You Work For

This is less of something to do and more of something to learn. One of the biggest hurdles I’ve seen to a person living on less are two words: “need” and “deserve”. “I need my Netflix and Hulu accounts because my friends all use it”. “I need to take an Uber because public transportation would take twice as long”. “I deserve this night out because I’ve had a rough week”.

Don’t get me wrong, I think it’s important to enjoy your life as it’s happening. But people who can’t seem to live within their means no matter what will often use these words to convince themselves of the necessity of their poor spending habits.

It can seem like a hard lesson to learn but we don’t “deserve” anything in life and “need” isn’t something you find on Amazon.com.

3. Daily Budget

I’m a big proponent of tackling the psychology of living within your means but there are tools that can help. Like I mentioned above, I don’t think the typical budget where you set limits for each category of spending works well. That type of budgeting has two main problems:

Too Much Work

Taking the time to enter and categorize every transaction is too much for most people to keep up with. And with the typical style of budgeting, you might have to do this consistently for weeks before you see where you can make adjustments.

Humans Don’t Live Life Per Month

It’s totally unnatural for a person to plan out an entire month of their life. But that’s exactly what a budget usually requires. We are much more comfortable with the concept of a day or maybe a week as a recurring cycle. Because of that, tracking your spending during a day makes way more sense than over the course of an entire month.

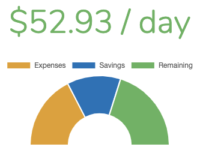

So how does a daily budget work? Basically, a daily budget takes your income, subtracts your regular expenses (like rent, insurance, etc), and divides that amount into the amount of dollars you have to spend each day.

Let’s look at an example:

Income: $2,000

Rent: $800

Car Insurance: $75

Income Minus Expenses: $1,125 (this would be your monthly budget)

Daily Budget (divided by 30): $37.50

In this very simple example, you would have $37 to spend each day on all your non-recurring expenses like food or transportation. You can immediately see how much you have and the end of the day is never very far away so you aren’t likely to feel like you’re falling behind.

A huge benefit to this method is that each morning, you have the same amount to spend. If you went over yesterday, you try something different today. The time between your purchase and knowing if it was too much or not will never be more than 24 hours.

The biggest advantage to this technique over any other budgeting styles is you can do it in your head. You don’t actually need any app or website to help you figure out whether your 3 purchase in the day was greater than that $37 (or whatever your number is).

That being said, if you WANT to use a tool, my recommendation is a daily budget app on your phone. If you search for “daily budget”, you’re virtually guaranteed to find a good one. I’ve tried this one on the iPhone and it was super easy to figure out and has an uncluttered interface (useful for keeping things simple). If you choose to use an app though, keep in mind that if it starts to feel like too much, ditch it. If you can add/subtract, you don’t need any app or website.